Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

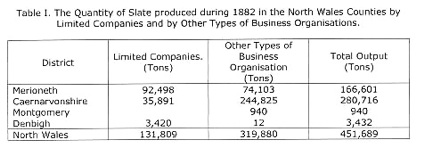

It would be difficult to overestimate the importance of the Companies Act of 1862 in promoting slate quarry enterprise. Under this Act any seven or more associates might constitute themselves a company, either with limited or unlimited liability, by simply subscribing a memorandum of association. Even after the passing of the Act there was some reluctance in many industries to adopt modifications in the traditional type of business organisation, a reluctance which the tardiness of the State to permit any general system of limited liability had encouraged; this was not the case with the slate industry. Table I shows the extent to which this form of organisation had been adopted in the industry by 1882, or twenty years after the passing of the Act.

In 1882 in Merioneth fifteen out of the twenty-five business units engaged in slate mining and quarrying were joint-stock limited liability concerns producing nearly 55 per cent. of the output of slate in the county and employing nearly 60 per cent. of the quarrymen. Out of thirty-six business units in the Caernarvonshire slate trade fifteen were limited companies which produced an eighth of the output and employed one-seventh the quarrymen in the county; in interpreting the statistics for Caernarvonshire it has to be remembered that the Penrhyn and Dinorwic concerns, together produced 198,595 tons valued at £468,212 and employed 5,566 men. In Montgomeryshire there were two small co-partnership concerns; in Denbighshire a limited company worked one quarry on a small scale. Taking North Wales as a whole we find that thirty-one out of sixty-five business units engaged in the exploitation of slate resources were limited liability companies employing more than a third of the total number of quarrymen and producing a little less than a third of the total output of the area.

The slate industry cannot be accused of being dilatory in adopting this new form of business organisation, especially the slate mining districts of Merioneth where economic penetration by English capital had been carried a stage further than in any other slate producing district.

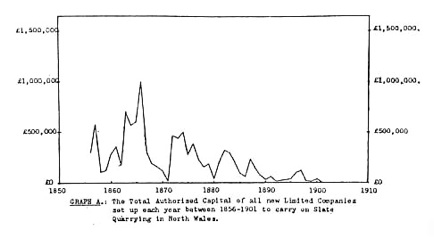

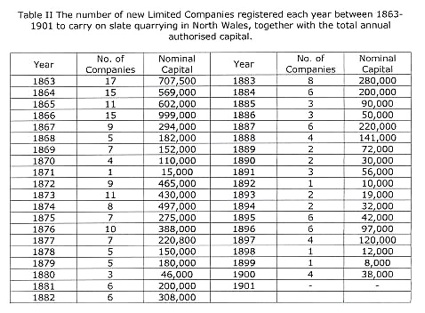

A good indication of the general trend in new capital investment in the industry from 1856 to 1901 is given by Graph A. The data upon which this graph is based is set out in Table II, except for the period 1856 to 1862 for which the relevant data appeared in Table II of last month's article. The graph does not set out to depict accurately the volume of new capital attracted each year to the industry in North Wales; it is based on the authorised capital of new limited companies registered in each calendar year and, consequently, it merely gives a very rough indication of the trend in investment.

Graph A. The Total Authorized Capital of all new Limited Companies not up each year between 1856-1901 to carry an Slate Quarrying In North Wales.

Graph A The total Authorised Capital of all new Limited Companies set up each year between 1856 - 1901 to carry on slate quarrying in North Wales.

It is rather interesting to note to what extent the cycle in investment in slate quarrying coincided with the cycle of building activity, and to note the relationship between them. Exceptional bursts of building activity in the mid-'fifties and mid-'sixties are reflected in contemporaneous booms in investment in slate quarrying. In 1866 when unemployment among carpenters and builders was .2 per cent, the authorised capital of fifteen new limited companies formed in that year to work quarries in North Wales amounted to nearly a million pounds, a record never since equalled.

Following the economic crisis of 1866 trade generally became sluggish and there was a minor cyclical setback in building, and a marked fall in slate quarrying investment. Recovery in building activity became very marked in 1872 and until the beginning of 1878 the industry experienced a period of feverish activity, especially in the provinces. The slate industry enjoyed several years of abnormal prosperity. Between 1870 and 1876 the prices of slates advanced upon the average 50 per cent. The demand was greatly in excess of the supply. As a consequence even large and regular customers of the quarries had to place their orders a long time beforehand, and merchants were anxious to contract for the whole output of the smaller concerns. So clamant and insistent was the demand for slate that merchants were obliged to send "blind invoices"; merchants sent orders for truck-loads and cargoes of slates without specifying sizes or qualities in the hope of quicker delivery. In 1876, on account of the abnormal state of the market, the small quarries which shipped their slates from Caernarvon were able to exploit the situation and charge prices 20 per cent. higher than the Penrhyn and Dinorwic quarries.

The general economic depression that began in 1875 did not fully affect building until 1878 when it was accentuated by several big disputes, notably the strike at the Law Courts. Unemployment in building increased from .7 per cent. in 1876 to 8.2 per cent. three years later. Most of the larger provincial towns, more particularly in the Midlands and the North, had been overbuilt and the building trades were now at a standstill. . In Glasgow the value of approved building plans fell from £1,269,000 in 1876 to £93,000 in 1879. The demand for slate had slackened .considerably in the latter half of 1877, and in November a general decrease in slate prices took place in the Caernarvonshire quarries; Festiniog quarries were able to maintain their prices, chiefly. because of the flourishing state of the export trade in which the Festiniog group of quarries had specialised, but in the following year demand was failing rapidly in all districts and prices came tumbling down with the result that the industry became acutely depressed. This depression, as is shown on the graph, had drastic repercussions on the volume of new investment.

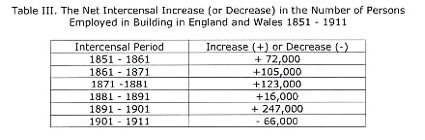

In 1851 and 1882 the tide once more began to turn with a slight improvement in building activity, but building remained at a low ebb throughout the 'eighties and, as was to be expected, the volume of capital investment in slate quarrying was much lower in the 'eighties than in the more prosperous ‘seventies. The early 'nineties ushered in a period of hitherto unparalleled building activity and during this decade, as is indicated in Table III, the expansion in the labour force of the building industry broke all previous records.

The most startling fact that the Table brings out is the unprecedented expansion in the labour force during the 'nineties, when nearly a quarter of a million more persons were attracted to the building industry than in the previous decade, and more than twice as many as in the booming 'seventies. This phenomenal expansion in building led to prosperity in the slate industry but, rather surprisingly, it did not lead to a great increase in investment in the industry; indeed, the volume of new investment in the 'nineties in North Wales was less than in the depressed 'eighties.

The absence of an investment boom in slate quarrying in the 'nineties despite boom conditions in building presents us with a nice little problem. Several explanations can be offered. In the first place a word of warning against regarding our graph as too accurate an index of the volume of new investment. The data upon which the graph is based is the nominal capital of new limited companies registered each year to carry on slate quarrying in North Wales. Some of these companies were stillborn; with many others the nominal capital was never subscribed up to the authorised limit; several other companies were old-established concerns who had been carrying on as partnership concerns or joint-stock companies with unlimited liability and which were merely being re-constituted on a new basis. The joint-stock limited liability form of organisation was often adopted when it was desirable to extend the quarries with lessened risk, when the entrepreneur grew old and wished others to share in the responsibility of managing and working the quarries, and when new capitalists took over the quarries to work them on a more ambitious scale. The history, of the formation of the Oakley Slate Quarries Company, Ltd., is fairly typical. Mr. Oakley, the owner of the mineral rights, had leased parts of his property to three concerns - the Upper Quarry to Mr. Holland, the Rhiwbryfdir Quarry to Mr. Matthews, and the Palmerston Quarry to the Welsh Slate Company. When the leases of the Upper and Rhiwbryfdir Quarries terminated in 1877 Mr. Oakley decided to take them over and to work them himself as they were extremely profitable concerns. He borrowed £50,000 from the Rock Insurance Company and £20,000 from Hoare and Company Bankers, to enable him to work the quarries. Unfortunately the boom in the slate industry collapsed and Mr. Oakley found himself in a difficult financial position and was anxious to get out of the responsibility of working the quarries. Messrs. Hoare and Company immediately offered to find all the capital Mr. Oakley might think necessary. They formed the idea of a company to be composed of members of the Oakley family and a few friends. Accordingly in 1882 the Oakley Slate Quarries Company, Ltd., was floated with an authorised capital of £255,000 in shares of £5,000 to take over the Rhiwbryfdir and Holland's Quarries; in 1889 it took over the Palmerston Quarry when the lease of the Welsh Slate Company expired. This history of this company shows that it was a slump in the slate industry, rather than a boom, which led to its formation in 1882. Financial retrenchment and capital reconstruction on the part of this and several other concerns was partly responsible for the slight boomlet in company promotion in the early 'eighties.

It would appear that the absence of a boom in company promotion in the ‘nineties was not attributable to any one simple reason but, rather, was the cumulative result of a complex of causes which all contributed in varying degrees to damp down enterprise. The most prosperous period in the history of the industry had been the thirty years up to 1878. Prices were rising; the demand, both domestic and foreign, was steadily increasing and was consistently ahead of supply. The larger concerns, such as Penrhyn and Dinorwic, were earning exceptionally high rates of profits. Consequently the slate industry came to be regarded as one of the most desirable fields for the investment of new capital. In the ‘sixties we find scores of new companies being registered each year to carry on various lucrative activities such as cotton spinning or coal mining, and, significantly enough, registering slate quarrying as one of their possible activities. Whether these companies did actually sink capital in the slate industry is doubtful but the inclusion of quarrying among their possible activities indicates in what high esteem the industry was regarded by the speculators of that period. Then in the 'eighties we have a period of stagnation in building, and of depression, over-production, and cut-throat competition in the slate industry, and the attraction exercised by the industry over the imagination of the British investor was rudely, and permanently, dispelled. The great building boom in the 'nineties brought new vitality into the industry but it did not regain favour in the eye of the investor. Up until 1877 the upward trend in slate production in North Wales had been very marked but, after falling in the ‘eighties, production did not rise in the 'nineties even to the 1877 level. The foreign demand for Welsh slate was falling in the 'nineties, the export trade having reached its high water mark in 1889 when 80,000 tons of slate was sent abroad. Foreign competition in the home market had begun to rear its ugly head. Prior to 1895 the import of slate into this country had amounted to some few hundred tons, but imports increased to 20,000 tons in 1895 and 120,000 tons in 1903. Another factor which tended to discourage new capital was the prevalence of industrial strife in the industry. There was a strike for 270 working days, from September, 1896, to August, 1897, at Penrhyn, which was the largest concern in the industry ; in the same concern another industrial dispute flared up in 1900 and actually lasted for three years. These unfortunate and protracted disputes had a detrimental effect upon the economic position of the industry as a whole because they prevented a rise in slate production when demand was expanding and so provided an ideal opening for foreign competitors and acted as an added stimulus to the production and use of substitutes. Still another factor was that by the end of the century practically all the productive slate veins in North Wales had already been tapped and had either been worked out or were in process of being worked by an existing concern. Geological considerations set a limit to the number of business units which can profitably be set up in an extractive industry, such as quarrying. The above were the main factors which jointly explain the lack of interest shown in the industry by the British investor at the turn of the century.

Investment in the Slate Industry 1830 - 1930 Part 3

Quarry Managers' Journal March 1943

First series

Investment 3

Second series

Third Series

Other slate information

National archive slate records

Links

Oakley quarry 1910