Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

In last month's issue we quoted the interesting proposals for the reorganisation of the slate industry made by the North Wales Quarrymen's Union in a memorandum which it has presented to the Welsh Reconstruction Advisory Council. This memorandum also gives an admirable survey of the history of the industry during the past half a century as well as a penetrating analysis of the factors underlying the contraction in the industry since 1898. In this issue we are again reproducing long extracts from the memorandum for the benefit of our readers.

Historical Retrospect

"The bare outline of the history and developments in the slate industry of North Wales is brought out in Table A., which gives the number of Business Units, the number of employed quarry-men and the annual output of slate in North Wales for certain years between 1885 and 1937.

"The history of the slate industry in North Wales falls into three distinct stages. A period of steady expansion and great prosperity ended in 1878. This was a period of great speculative activity with a great volume of new capital being sunk annually in the industry. The second period was one of instability with the industry passing from acute depression in the 'eighties' to moderate prospErity in the late 'nineties' when output was slightly lower than in the 'seventies.' In this period only a very limited amount of new capital was attracted, and it was characterised by financial re-organisation on the part of many existing concerns. The third period has been one of contraction and, as Table A shows, the output of the industry prior to the present war was only slightly more than half what it had been at the end of the last century. The contraction was very rapid in the fifteen years preceding the last war. The Great War paralysed the industry and, consequently, there was a great exodus of workers to work in coal mines, munition factories, and to join the Armed Forces. After the Armistice the industry recovered somewhat and output increased slowly until 1927 when 252,273 tons were produced. The 1927 level of production was some 43,000 tons below that of 1913. From 1927 until 1939 the trend in production has been slightly downwards. With the outbreak of hostilities production slumped as in the last war.

The Slate Industry 1898 - 1918

"The contraction of the slate industry during this period was mainly attributable to the great depression in the building industry after 1903.

"The 'nineties' had been a period of hitherto unparalleled activity in building, but the opening decade of the new century brought with it a new phase in the history of the building industry. It is practically certain that no net decrease in the labour force of the industry occurred during any decade in the Nineteenth Century, but between 1901 and 1911 the number of building operatives fell from 953,000 to 887,000, showing a net loss of 66,000 workmen. By 1905 unemployment among carpenters and joiners was as high as 8 per cent.; only twice in the black years 1879 and 1886 had unemployment among carpenters exceeded that level since unemployment statistics were first compiled in 1860. By 1909 unemployment had reached the unheard of level 0f 11.7

"The Great War virtually crippled the building industry. Building was impeded by financial stringency, increasing scarcity and rising cost of materials and labour, and an Order issued by the Ministry of Munitions in July, 1916, prohibited in all cases involving an outlay of over £500, the construction, repair, alteration or decoration of buildings except under licence. Consequently, residential construction was reduced to a tiny trickle after 1916.

"In view of this prolonged and acute stagnation in building activity, a reduction in the volume of slate production was only to be expected.

The Slate Industry 1919 - 1939

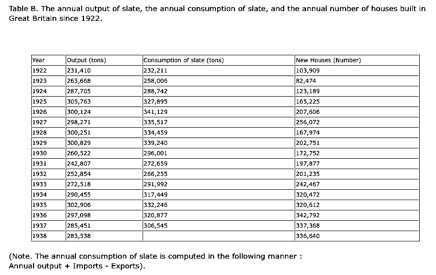

(Note. The annual consumption of slate is computed in the following manner : Annual output + Imports - Exports).

"Table B. shows the exceptional expansion in residential building activity, especially after 1924. The volume of building broke all records in the inter-war period, and one would expect a great contemporaneous expansion in slate production. The annual slate production reached its highest point in 1925 and the volume of slate consumption was highest in the following year. It is highly significant that in 1924 and 1925 the building boom was only in its early stages; the rate of building in those years was less than half what it was after 1933, and yet the volume of both slate production and slate consumption was substantially higher than in the later period.

Factors Affecting the Economic Position of the Industry in the later war Period

“I. CHANGES IN THE TECHNIQUE OF NON-RESIDENTIAL CONSTRUCTION.

Whereas before the last War practically all factories, shops, business premises, and public buildings had sloping roofs of slate, it has become increasingly the practice for non-residential buildings either to have flat reinforced concrete roofs or else sloping roofs covered with glass, asbestos sheets or tiles, or some roofing material other than slate.

"II. THE BALANCE OF IMPORTS AND OF EXPORTS.

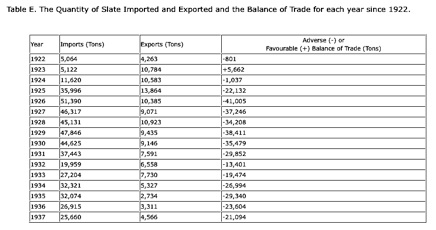

Table E. The Quantity of Slate Imported and Exported and the Balance of Trade for each year since 1922.

Note: Tables B and C do not appear in the original publication.

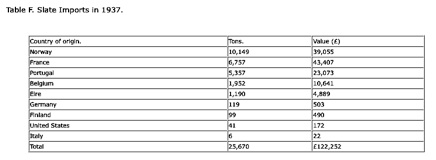

"In the inter-war period the volume of imports reached its highest point in 1926 when 51,390 tons were imported, of which some 35,000 tons came from France. Since 1929 there has been a marked downward trend in imports, mainly because of the fall in imports from France. The source of slate imports in 1937 Is shown in the next column.

"The most important development in the import trade during the decade preceding the outbreak of war was the almost uninterrupted growth in the import trade from Norway which rose from 83 tons in 1923 to 10,149 tons in 1937.

"Comparative prices are the decisive factor in the competition between home and foreign slates and it is a noteworthy fact that since 1923 the average price per ton (including cost of transport to this country) of imported slate has been substantially lower than the average price per ton of home produced slates on the quarry bank. The competition of foreign slates is especially keen in districts far away from slate producing areas, because railway rates are very high as compared with water transport. That this factor is important is indicated by the fact that of the total of 25,670 tons imported in 1937 only 210 tons were imported into Wales. Furthermore, practically all the Norwegian slates went to Newcastle, Leith and Grangemouth, whereas Grimsby, Harwich, Plymouth, Portsmouth and Southampton were the main importers from France and Belgium.

"Foreign slates are inferior in quality to the home product and there are many instances where foreign slates, after being exposed for a few years to the acid laden atmosphere of our great industrial cities had decomposed to such an extent that they have had to be stripped and replaced with Welsh slates. Much of the imported slate is, however, used as damp course in laying the foundations of buildings.

"The export trade in slate has sunk into a very low level since 1925 when 13,864 tons were exported, of which 9,490 tons went to Eire. The fall in subsequent years has been due to a contraction in the Irish market, due to subsidisation of the Irish industry, and the imposition in 1934 of a heavy tariff against imported slates. Practically all the slate exported from this country comes from North Wales.

"III. DECLINE IN THE OUTPUT OF SLATE GOODS.

According to Census of Production Reports the total value of slate goods (mantels, chimney pieces, writing slates, etc.) was £219,000 in 1924 and £172,000 in 1935. In the latter year the total value of slate production (excluding rough slate used for walling or as road metal) was £1,730,975.

"English production rose both relatively and absolutely between 1925 and 1935, see Table G shown in next column. This was due partly to the growing preference shown for the 'architectural,' 'rustic,' and the Green slates which are produced in the south west of England and in the Lake District. Partly also to the development of motor transport which has formed a close link between out of the way quarries and the market. In the same period Welsh production fell, chiefly because of the contraction which took place in the output of the slate mining district of Merioneth.

"In 1935 Wales produced 75% Of the total home production, and 87% of the total in value. The roof covering capacity of the North Wales output of slates is greater than the 75% referred to above. The Welsh slate is thinner and, therefore, there are more slates to the ton. Its roof covering capacity is nearer 85% to 87.5%"

"IV. GROWTH IN THE RELATIVE IMPORTANCE OF SLATE PRODUCING AREAS OUTSIDE WALES

It is pointed out in the memorandum that, important as the four causal factors mentioned above are, the main cause of the contraction in the slate industry was the phenomenal growth of the roofing tile industries during the inter war period. In our next issue we propose to quote that section of the memorandum which shows how "In the persistent tug of war between the various types of roofing materials for supremacy in the market, as influenced by economic, aesthetic and technical factors, the slate industry has been decisively challenged by the roofing tile industry.

Aspects of the Slate Industry 2: Causes of Contraction in the Slate Industry

Quarry Managers' Journal June 1943

First series

Second series

Causes of contraction

Third Series

Other slate information

National archive slate records

Links