Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

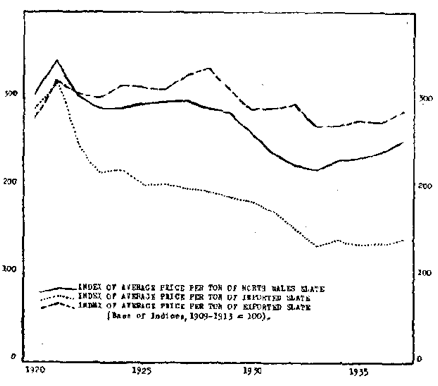

In the concluding paragraph of our last article it was pointed out that in 1937 the average price per ton of imported slate was Only 41 per cent. higher than during the quinquennium 1909 to 1913, whereas in the same, year the average value per ton of slate produced in North Wales was 152 per cent. higher and the average price per ton of slate exports was 187 per cent. higher.

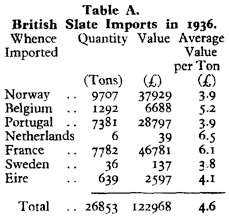

These divergent trends in price levels are brought out in the graph. Attention has been drawn in a previous article to the qualitative changes in the export trade, changes which are reflected in the inflated price index. There were also contemporaneous qualitative changes in the import trade but they were not comparable in magnitude to those in the export trade. Table A shows to what extent the average value per ton of slate imported from various countries varied in 1936.

The most expensive slates were imported from France and following 1930 imports from that source were reduced, whereas imports of the less expensive slates from Norway and Portugal were increased and this qualitative change in the nature of the import trade was sufficient of itself to bring about a reduction in average prices, without actual price lists being affected at all. This point illustrates the unreliability of price statistics based on "average" prices of imports and exports, either as a basis for comparison or as a criterion of the actual movements in price lists. Such statistics have to be used with the utmost circumspection and great care has to be exercised in interpreting them.

After making full allowances for the limitations of the data plotted on our graph it is abundantly clear that there was a marked downward trend in the prices of imported slate in the interwar period and that the foreign product was substantially cheaper than the British product on our domestic market. In 1936 the average value per ton of British slate was £5 16s. 8d.; the average value per ton of imported slate in that year was £4 11 8d. less by £I 5s. 0d. per ton and it has to be borne in mind that the value of the imported slate is based on c.i.f. prices, whereas the value of British slates is based on prices on the quarry bank. In pre‑war days best quality green Norwegian slates were about ten per cent. cheaper than best quality Welsh slates and about forty per cent. cheaper than the green slates of Cumberland and Westmorland. On a comparative price basis the imported slates were sold at an uneconomic level, judging by the standard of costs in our home industry, and it is little wonder that the foreign product found a ready market, especially in those districts far distant from the home producing areas.

We will now proceed to deal with the question as to the nature of the tariff policy which those interested in the British slate industry should advocate in respect of their particular product. We all remember the heat that was engendered by the public controversy on the subject of tariffs on imports, which took place at the time of the economic blizzard which swept over the world in the early 'thirties. There were two main schools of thought at that time. There was the school of thought who maintained that tariffs would reduce imports and the reduction would be made good by increased production at home, giving increased employment ‑ therefore tariffs were said to be a good thing. The other school maintained that tariffs would reduce imports and reduce the capacity of other countries to buy our goods, thereby reducing employment in the exporting industries ‑therefore tariff., were a bad thing. Both schools of thought indicate correctly the conflicting results of tariffs but neither school of thought seems a reliable guide because the one concentrates exclusively on the favourable results and the other school concentrates attention wholly on the unfavourable results of tariffs, whereas the truth can only be arrived at by attempting to access the relative importance of the favourable and unfavourable effects. Then there was the general, but unreasoning, temptation to which most people succumbed of becoming either rabid Free Traders or fanatical Protectionists, whereas it is more sensible to be both at one and the same time. One can believe strongly at one and the same time that there should be free‑trade in bananas, or wheat, and believe equally strongly in protection for cotton goods, slates, etc. The day is past when the issue of Free Trade versus Protection has to be settled in terms of industry and agriculture as a whole; it has to be settled in terms of each individual, industrial and agricultural products, and it is on that basis that we intend to deal with this issue for the state industry.

The author every day has occasion to pass a cluster of modern semidetached houses, of which all except two are roofed with the familiar "boiler‑plate" variety of tiles. The other two houses are roofed with states and stand out in marked contrast to the rest. Sad to relate, the conspicuous roofs of these two houses are in a deplorable state because the acid‑laden atmosphere of the district has caused the slates to disintegrate ; all the states have flaked badly and will have to be replaced in the near future. the slates are indistinguishable in appearance from the so‑called "Portmadoc" slates produced in the underground workings of the Festiniog district of Merionethshire. Portmadoc slates are world‑famed for their durability and they have never been known to disintegrate in this fashion. Obviously these two houses were roofed with inferior French slates, which are almost indistinguishable in appearance from Portmadoc slates and which were extensively imported during the 'twenties and used by speculative builders who were more concerned with the cheapness of the roofing material than with its durability.

Most of the slate imported into this country is decidedly inferior in quality to the British product. There are literally hundreds of houses which have been roofed with foreign slates and which have had to be repaired and finally re‑roofed with British slates. On the other hand, there is not a single instance of home‑produced slates disintegrating in this fashion, even after being exposed to the corrosive atmosphere of our industrial towns for several decades. A substantial proportion of the inferior foreign product was used as damp‑course in the foundations of houses, but it was also used on a large scale for roofing purposes. Our home industry undoubtedly produces a better quality product so that the exclusion of foreign slate from the British market would mean the exclusion of an inferior article. That is the first point to be borne in mind. The second point that is relevant to our argument is that the proven inferior quality of imported slate reacts to the detriment of slates in general, and the worse possible advertisement for the British slate industry is the sight of a disintegrating roof of foreign slates. This sort of spectacle creates a prejudice not only against foreign slates but against our domestic product as well.

A third point is that the importation of foreign slate greatly accentuated the depressed state of the British slate industry in the inter‑war period, especially in the 'thirties.

The Welsh industry is largely localised in the Bethesda (Penrhyn Quarries), Llanberis (Dinorwic Quarries), and Nantlle districts of Caernavonshire and in the Festiniog district of Merioneth. Few people realize the extent to which the Welsh slate producing areas are dependent upon this industry. It is frequently tacitly assumed that in the above areas there are important minor industries and that, taken together, these small and diversified occupations are more important than the mining and quarrying of slate. That such an assumption is perfectly erroneous is clearly indicated by the fact out of a total of 9,610 insured persons aged 16 to 64 years in those four areas in July, 1937, as many as 7.300 were employed in the slate industry. In these areas the slate industry is several times as important as all other insured trades and occupations put together.

This fact has two main corollaries. As there were no important minor industries in the quarrying districts and as the slate industry is an exclusively masculine occupation, it follows that there is an abnormal preponderance of male over female labour.

In 1937 only 1 out of every 27 insured persons was a female in the Welsh slate valleys, as compared with an average of 1 out of over 4 for Great Britain as a whole. In the slate valleys the welfare of almost every household is wholly dependent upon the wages earned by the men‑folk. The other corollary which follows from the fact that more than three quarters of the insured population of the Bethesda, Llanberis, Nantlle and Festiniog districts are employed in the slate industry, is that the prosperity of these areas is conditioned almost wholly by the prosperity of that one industry. It is an established historical fact that the population of these districts fluctuates with the volume of slate production and that the great contraction which has taken place during the current century in the slate industry has led to a great contemporaneous decline in the population of the quarrying districts. This excessive dependence upon one basic industry has led to very great hardship in times of trade depression ; e.g., in May, 1931 74 per cent. of the insured workmen in the Llanberis district were temporarily unemployed because of the slump in the slate industry. In these areas there are no subsidiary and supplementary industries to act as buffers when the slate trade was stagnant.

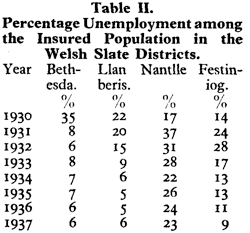

Table II shows how these Welsh areas fared as regards unemployment during the 'thirties.

These unemployment statistics reflect a bad state of unemployment, especially in the Nantlle and Festiniog slate districts which suffered from chronic unemployment in a very acute form, many quarrymen having been out of work for more than a decade

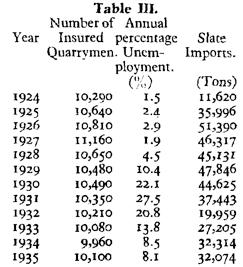

Table III shows the changes in the estimated number of insured workpeople in the British slate industry for each year from 1924 to 1935 inclusive and also the average annual percentage unemployment in the industry during that period, as well as the annual quantity of slate imported into the country. Unemployment was very prevalent in the slate industry after 1928, and during those depressed years foreign slate continued to be imported on a large scale. The average annual per capita output in the home industry is about 30 tons of finished slate and on this basis we can estimate that the production of the 44,625 tons imported in 1930 would have provided employment for nearly 1,500 quarrymen and the 32,074 tons imported in 1935 would have provided work for over I,000 quarrymen.

It does not follow that orders for foreign slate would be automatically transferred to British slate producers if importation was prohibited. Some of the orders would undoubtedly be placed with tile manufacturers but, on the other hand, it is indisputable that the imposition of a prohibitive tariff would materially increase the demand for British slate and would provide work for several hundreds of unemployed quarrymen.

Unemployment was a terrible scourge in the Welsh slate valleys because there were no other local industries which might provide alternative employment, and to allow the importation of inferior foreign slate while chronic unemployment was rampant in the British slate industry was to carry economic orthodoxy to extremes. Charity begins at home and, by excluding imports, we would increase employment among British quarrymen (and clay workers) and so increase the purchasing power of these workers by at least as much as we decrease the purchasing power of foreign quarrymen ; the exclusion of foreign slate would certainly benefit not only the British slate industry but other industries as well. The degree to which this would affect our export industries is problematic, but it can be said that any adverse repercussions would be more than compensated for by the beneficial effect on other industries.

There are several other points that might be elaborated upon in the development of our argument – the liquidation of our own export markets, that the exclusion of foreign slates would make it easier to eliminate cut throat competition within the industry, the tonic effect that protection would have in restoring the investor's faith in the future prospects of the industry, etc. To import slate to this country is worse than carrying coal to Newcastle and it is suggested that those interested in the industry should demand full protection against the foreign competitor in post‑war days.

Aspects of the Slate Industry 10: Free Trade versus Protection

Quarry Managers' Journal February 1944

First series

Second series

Free trade vs protection

Third Series

Other slate information

National archive slate records

Links

Dividing blocks Penrhyn quarry 1925