Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

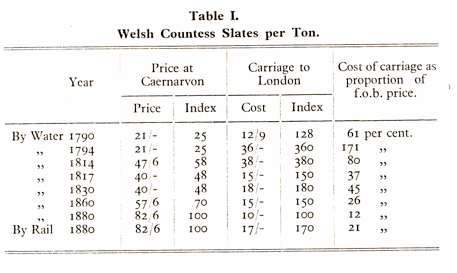

Certain important factors which materially contributed towards an expansion in the demand for slate are brought out in Table I. below which shows, for various dates between 17go and 1882, the f.o.b. price per ton of Countess (20 X 10 ins.) slates at the port of Caernarvon, together with freight cost per ton to London.

The above table shows that, with the exception of the time of the war. with France when freight rates were abnormally high, the proportion which transport costs bore to the price of slate was progressively lowered; the cost of sending slate by water from Caernarvon to London, expressed as a percentage of the value of the product at port of lading, amounted to 61 per cent. in 179o and 12 per cent. in i88o; in the later year, if the slate was forwarded by rail the proportion was 21 per cent. This relative decline in the importance of costs of transport contributed powerfully towards an expansion in demand for slate.

The outbreak of war with France in 1793 had brought with it a remarkable increase in freight rates from the slate ports of North Wales, particularly along the London route along which war risks were greatest. In the deflationary period which immediately followed the termination of war, freight rates slumped and then for nearly half a century they fluctuated around a fairly stable level. There was another marked fall in water‑carriage between i86o‑8o as the competition between the railways and coastal shipping became very keen in the late 'sixties.

The cost of shipping slate from North Wales to the London market was only 2/9 per ton cheaper in 1880 than in 1790, whereas the cost of a ton of Countess slates at Caernarvon had increased by 61/6 during the same period; it is therefore clear in the case of the coastal markets that the pronounced decline in the relative importance of the cost of transport to market as compared to the value of slates at port of lading, was due mainly to the rise in the price of slates rather than to the fall in freight rates. The fall in the cost of inland carriage between 1790 and 1880, as the result of the construction of canal and railway systems, was much more considerable than the contemporaneous fall in the cost of water carriage and was the chief factor in opening new markets for the sale of slate; in the case of inland markets the lowering of the proportion which transport costs bore to the value of slate was due even more to the fall in the former than to the rise in the latter. Before the coming of canals and railways a large inland market for slate was out of the question because of excessive costs of transport.

Railway freights, as is shown in Table 1. were substantially heavier than water freights but the. railway had several important compensating advantages, such as quicker and more prompt delivery, fewer breakages in transport, the elimination of much loading and unloading, and the case with which orders for small quantities of slate could be executed. One by one the major slate ports had been linked up with the general railway system - Port Penrhyn in 1848, Port Dinorwic and Caernarvon in 1852, Portmadoc in i967 ‑ and the competition between the railways and coastal shipping brought freight rates down on land and water; of greater consequence was the economy effected when, as was frequently the case, it was cheaper to send slates direct to inland towns rather than along the more circuitous water route by which the slates had been shipped coastwise to a convenient port and there transferred into barges or railway trucks to be conveyed inland.

Throughout the period under consideration slates were increasing in popularity and the determining factor was the comparative all‑in cost of roofing with slate and with competitive materials. Despite the fact that the general level of prices displayed a pronounced downward trend from 1809 to 1849, the contemporaneous trend in slate prices was slightly upwards; during the following thirty years the indices of wholesale prices and of slate prices both showed a marked upward trend. If we consider the first three‑quarters of the century as a whole, we find that the trend in the general level of prices was downwards whereas that in slate prices moved in a contrary direction. It has to be remembered, however, that the index of slate prices represents the f.o.b. or f.o.r. prices at point of shipment, and in comparing the actual cost of slate at different periods at the place where it was used, allowance has to be made for the economics which took place in the cost of transporting the commodity to market, and for the repeal of the heavy tax which was levied on slate carried coastwise between 1794 and 1831.

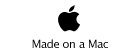

Table 11. shows for various dates an index of slate prices, together with the comparative costs, including cost of materials and labour, of roofing 100 square feet with slates and with tiles respectively in the London market. The variety in the quality and sizes of both slates and tiles makes it difficult to obtain strictly comparable statistics of the respective costs of slating and tiling; another complicating factor is that tiles could be laid on a roof showing either 3, 3½ or 4 inches on face and slates could be laid with a lap of anything between 2 and 4 inches and this diversity in roofing practice led to variations in the all‑in cost of roofing. In the table below the cost of slating is based upon the all‑in cost of roofing with Welsh Countess slates laid to a 2½ inch lap; the cost of tiling is based upon the all‑in cost of roofing with plain tiles showing 3½ inches on face; these two series form accurate indices of the average cost of slating and tiling respectively, and are sufficiently representative to be used for comparative purposes.

The Table below demonstrates clearly that, although there was a great increase over this period in the f.o.b. price of slate, the all‑in cost of roofing with slate in the London district was 21 per cent. higher in 1805 than in 1880. During the first thirty years of the century the cost of slating was swelled by expensive costs of transport and by the heavy ad valorem duty on slates carried coastwise (the incidence of which was heavier the more distant the market), but in the 'thirties and 'forties there was a substantial fall in the cost of slating as a result of the abolition of the slate tax, improvements in transport facilities and, to a much smaller extent, the fall in the cost of nails and laths. [1] The index of the cost of slating fell from 118 in 1825 to 70 in 1845, and then rose steadily and gradually to 93 in 1870; it rose sharply to 138 during the great boom in the 'seventies and then declined to 100 in 1880.

From 1825 to 1880 it was much cheaper to roof with slates than with tiles, except between 1875‑77 when the abnormal demand for slates raised prices to such a level that the cost of tiling was less than 1 per cent. dearer than the cost of slating; slating was cheaper than tiling by 80 per cent. in 1845, 55 per cent. in 1855, 45 per cent. in 1865 and 39 per cent. in 1880. These statistics relate to the comparative costs in the London district of roofing 100 square feet with Welsh Countess slates and with local plain tiles respectively; roofing with tiles brought to London from Staffordshire was much more expensive than with plain tiles which were produced locally; we find that in 1880 Staffordshire tiling cost 69/3 per 100 square feet as compared with 59/3 for plain tiling and 35/6 for Welsh slating. In view of the very wide margin between the comparative costs of slating and tiling it is not difficult to account for the growth in the slate industry.

During the first quarter of the century the margin between the costs of roofing with local tiles and Welsh slate respectively in the London market was very small owing to the crippling effects of high freight rates and the burdensome slate tax. The termination of war brought with it a pronounced reduction in freight rates and a reduction in the slate duty, with the result that an upward trend in slate production once more becomes very apparent. The margin between the cost of slating and tiling in London increased from less than 1 per cent. in 1805 to 10 per cent. in 1825 and as early as 1822 we learn that "The great durability, lightness [2] and cheapness of a covering of good slates, compared with London tiles, has of late years been operating towards gradually diminishing the demand for tiles in London and its vicinity." It is interesting to note that in the early 'twenties the Trimmer family, which for over a century had been among the largest manufacturers of tiles in the country, went to considerable trouble and expense to obtain possession of a slate quarry adjacent to the renowned Penrhyn Quarry; in their application to the Crown for a lease of the quarry it was pointed out that their long‑standing connection with the tile industry placed them in an advantageous position for the large‑scale exploitation of slate resources as "Those who have hitherto most extensively supplied the tiles, have of course the commercial connections ready formed through which slates could be substituted and that in an increasing degree, as the interest of the seller was promoted by the substitution."

1 The cost of shipping a ton of slates from Caernarvon to London fell from 35/‑ in 1805 to 20/‑ in 1825 and to 15/- in 1845; the duty payable per ton of Countess slates at London fell from 20/‑ in 1805 to 11/3 in 1825 and had been abolished by 1845; the f.o.b. price per ton of Countess slates increased from 27/6 in 1805 to 45/- in 1825 and 1845. It will be seen therefore that between 1805‑45 the cost per ton of Countess slates had increased by 17/6 whereas the cost of carriage to London and the amount of duty per ton had together fallen by 40/‑ in the same period.

2 The extremely high price of timber during the Napoleonic Wars was one factor which encouraged the substitution of slates for clay tiles and stone states, as the former, being lighter in weight, required less roofing timber.

Aspects of the Slate Industry 13: The Expansionist Period 3

Quarry Managers' Journal May 1944

First series

Second series

Third Series

Expansionist period 3

Other slate information

National archive slate records

Links