Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

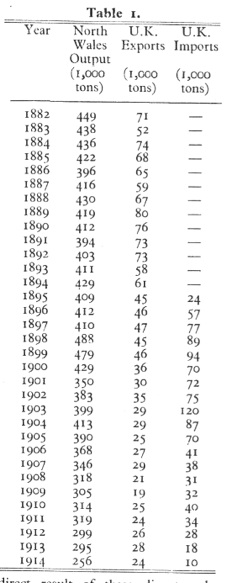

The great Penrhyn disputes of 1896-7 and 1900-3 had disastrous repercussions on domestic and foreign trade in Welsh slates. There was at that time a great and growing demand for slates as a result of boom conditions in building and it was of paramount importance to the slate industry, if it was to maintain its predominant position among the roofing material industries, that the output of slate should be increased as quickly as possible. The prolonged industrial disputes at the largest productive unit in the industry proved a great handicap, as is shown in the following Table. Table I shows the quantity of slate (excluding undressed slate which was used for walling, etc. produced in the mines and quarries of North Wales between 1882 and 1914; it also shows the volume of slate exports from Great Britain and the total volume of imports for each year during the same period. The output of slate for the years 1896 and 1897 would have been substantially larger were it not for the dispute at the Penrhyn Quarry. In 1898 the North Wales output increased by some 78,000 tons but the closure of the Penrhyn Quarry in 1899 caused a substantial decrease in output. In 1901 the total British production of slate fell by 94,000 tons - a fall exactly equivalent to the output of the Penrhyn Quarry in 1899. In 1902 and 1903 the Penrhyn Quarry was worked at about 45 per cent. of its capacity by non-unionists, and many of the strikers found employment in other quarries so that the output of slate recovered somewhat. As a direct result of these disputes the Penrhyn Quarry lost the proud position it had held for more than a century as the largest productive unit in the British slate trade. The Dinorwic Quarry has throughout this century ranked as by far the largest concern in the industry.

Lesson Number One

In our last article we quoted from official United States Reports and from an American technical journal to show how eagerly American state producers grasped at the golden opportunity afforded to them to push their wares abroad as a result of the unfortunate industrial disputes. We also showed from the official reports of the British Consul at Hamburg how badly the all‑important trade with Germany was bit, partly because British slate producers were diverting their product into the domestic market to replace the Penrhyn output and to satisfy the clamant home demand, and partly because the increase in prices, consequent upon the disparity between supply and demand, precluded exportation on a large scale to the German market. It is transparently clear that the Penrhyn disputes did permanent harm to the industry and the obvious moral is that in the slate industry there is an overwhelming case for the settlement of industrial disputes by arbitration, inasmuch as strikes and lockouts accentuate the forces which make for contraction. The slate industry, with its steadily rising costs of production, unprotected against foreign competition and exposed to the aggressive competition of all kinds of home produced substitutes, is the one industry in Great Britain which can least afford the luxury of prolonged industrial disputes. Employers and employed should rake this lesson to bout and realise, whatever may be the points at issue between them at any time, that the best interests of both parties will be served if these differences con he resolved by conciliation and not by resorting to strikes and lockouts.

A glance at Table 1 will suffice to show us that British slate exports fell from the record total of some 80,000 tons in 1889 down to some 29,000 tons in 1903, and that in the same period the volume of exports increased from a quantity too negligible to be separately recorded in the Board of Trade Annual Returns, to the very impressive total of 120,000 tons. How did it came about that such remarkable quantities of slate were imported between 1895 and 1905? The Penrhyn disputes but, if we are to preserve a proper sense of proportion, we mast conclude that these disputes were only an important contributory cause. Even if these disputes could have been avoided it is clear that very substantial importations of slate would have taken place, m a result of certain weaknesses inherent in the economic organisation of the industry. We must call in economic analysis once more to our aid and by means of it discern what lessons for to‑day can be learnt from past history.

The most amazing fact which Table 1 brings out is the comparative inertness of slate production in North Wales in the 'nineties. Building activity was stagnant in the 'eighties whereas in the 'nineties the building industry experienced the greatest boom in its history daring the nineteenth century and yet, even in the years when there were no strikes or lockouts, the volume of Welsh slate production in the prosperous 'nineties was very little greater than in the depressed ‘eighties. The root cause of this apparently inexplicable state of affairs is to be found in the chaotic organisation of the industry at that time, and this we shall now proceed to study in some detail.

Cut‑throat Competition

The demand for slate had revived somewhat after the slump year 1879 and this minor boomlet reached its peak in 1882 and led to such a substantial recovery in output that sales were only possible at prices varying between 30 and 45 per cent. (according to the discounts allowed off the price- list) below those of 1877; the benefits of the slight improvement in demand were more than neutralised by the disproportionate increase in supply, and this over-production was chronic throughout the 'eighties. Repeated attempts were made in that decade by the Welsh slate producers to decide upon uniform price-lists and to fix maximum rates of discount. These efforts at co-operative price-fixing proved futile and slate prices continued to fall throughout the 'eighties.

The Penrhyn and Dinorwic Quarries were determined to obtain what their entrepreneurs defined as a "fair" share of the market, which was actually interpreted by them to mean that share of available demand large enough to enable them to maintain the scale of their operations. Demand was inelastic and contracting and these two concerns, in their efforts to maintain the volume of their output, reduced prices and made additional concessions such as heavy discount rates, large over-counts, the sale of best quality slates for the price of inferior slates, and the disposal of particular sizes of slates in lots for extremely low prices as soon as they began to accumulate in the quarries. For over half a century these two major concerns had acted together in determining upon uniform prices but after 1882 they issued separate price lists, each complaining that the other was taking more than its "fair" share of the market by resorting to "unfair" methods of competition.

The slate produced in many of the smaller productive units in North Wales was inferior in quality to the product of the Penrhyn and Dinorwic Quarries and so did not command so high a price in the market, especially now that demand was slack (and possibly merchants and builders had long memories and remembered how in the great boom years 1876 and 1877 the small quarries in the Llanberis and Nantlle district had exploited the abnormal demand to such an extent that their prices were 20 per cent. higher than those of the Penrhyn and Dinorwic Quarries). During this period the initiative in reducing prices was taken by the Penrhyn concern, and each price change was followed by an approximately similar change in the prices of Dinorwic slate, and the smaller concerns were constrained to make even greater reductions. Prices came down in a vicious circle and they had been reduced to such a low level that in the first quarter of 1885 the Dinorwic Quarry, despite the advantages of large-scale production and of operation by the owner of the mineral rights, was worked at a loss. The officials of the North Wales Quarrymen's Union and many quarry proprietors were convinced that prices could be raised 15 per cent. without appreciably affecting volume of demand, and that the larger concerns were consciously pursuing a price policy calculated to close down the smaller productive units.

A prolonged lockout in the Dinorwic Quarry from October 31st, 1885, until March 1st, 1886, temporarily reduced the supply of slates and raised prices slightly and so provided some relief for those concerns which had been worked at a loss for many years. Quarry proprietors did not wish to close their quarries, even when they were unprofitable, as they tended to become derelict if they were left idle for more than a short period and many concerns struggled to survive the depression by doing only the bare minimum of un-remunerative work and concentrating upon the most productive parts of the quarries;

this policy could not be continued indefinitely and with a further break in prices after 1885, many quarries became idle and by 1891 there were in North Wales nineteen fewer slate mines and quarries in active operation than in 1885.

There was a very small increase in building activity between 1888 and 1891, but the output of slates in North Wales fell gradually during those three years, chiefly because of the closing down of quarries which had long been worked unprofitably ; other contributory causes were the occurrence of minor trade disputes in the slate mining areas of Merioneth and the fact that the slowly reviving demand was met, not by increasing production, but by depleting the heavy stocks which had accumulated at the quarries and by diverting supplies from the contracting foreign market to the home market. The Welsh entrepreneurs‑most of whom had been reduced to desperate straights‑made determined concerted efforts to reduce trade discounts and to eradicate aggressive selling methods; this renewed, and more successful, attempt at co‑operative regulation of prices, together with the gradual liquidation of overproduction through reduced production in the face of a reviving demand, introduced a firmer tone into the market and the. prolonged downward trend in prices (which had fallen 39 per cent. between 1877 and 1889) was finally checked in 1889; it was not until 1892, however, that any appreciable rise in slate prices occurred.

Impaired Productive Capacity

After a decade of cut‑throat competition and overproduction the position of the slate industry in the early 'nineties may be summarised as follows :‑

(1) Numerous concerns, after sustaining heavy financial losses, had been forced to close down, so that the productive capacity of the industry was drastically impaired.

(2) In all the quarries only the more productive parts had been worked and only the bare minimum of "dead" development work had been done. Judging from contemporary reports the quarries as a whole were in a parlous state and this again reduced the capacity of the industry to increase its output.

(3) The margin of profit had been reduced to very narrow limits in all cases (and was frequently non‑existent) so that the quarries had no accumulated reserves of capital which could be drawn upon to carry out the expensive task of once more developing the slate veins along scientific lines.

(4) Cut‑throat competition, frequent bankruptcies, the closing of quarries, widespread industrial strife (itself the result of the forcing down of slate prices), had gained the industry an unenviable reputation among the investing public so that there was little prospect of attracting outside capital to the industry to he spent on increasing its impaired productive capacity.

Lesson Number Two

It is little wonder, therefore, that, despite the intense building boom in the 'nineties, there was no marked increase in Welsh slate production, and at no point did the output conic up to the level reached in the 'seven~ ties. The productive capacity of the industry had been permanently impaired‑not by the Penrhyn disputes but by the chaotic marketing conditions which prevailed in the 'eighties. In some industries even cut‑throat competition sometimes serves,a useful social purpose because the less economic productive units are forced out of business and the larger units increase their output commensurately (and at decreasing cost), so that the productive capacity of those industries remain un-impaired. In the slate industry on the other hand, the elimination of weaker economic units has always meant a permanent decrease in the productive capacity of the industry and this together with the inability of any single productive unit in the industry (for obvious technical reasons) to increase its output rapidly, creates, during a building boom, conditions favourable to the importation of foreign slates and increased use of substitutes, and this reacts to the detriment of the industry as a whole. The same conditions apply today, except for that the struggle for survival has become more intense than at any previous time, and quarry proprietors should learn the lessons of the past and set up a marketing organization which will eliminate cut-throat competition and regulate production.

Aspects of the Slate Industry 7: Two lessons from the past

Quarry Managers' Journal November 1943

First series

Second series

Two lessons from the past

Third Series

Other slate information

National archive slate records

Links