Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

Historical aspects of the Welsh slate industry

D Dylan Pritchard MA FSS

One of the factors underlying the large‑scale importation of foreign slate during the inter‑war period was described in the concluding part of our last article. The slate producing districts of Great Britain are situated along the west coast‑Argyllshire, Cumberland and Westmoreland, North Wales, Pembrokeshire, Cornwall and Devon so that transport of slate to many parts of Britain involve costly cross‑country railway journeys. Conclusive evidence was given to prove that those heavy railway freight charges gravely handicapped the home producer in the more distant domestic markets. In the western and north-western parts of Britain the home producer is at a very great disadvantage compared with his foreign competitor, and the latter enjoys to the full the differential advantage he enjoys in the form of cheap water carriage.

In markets which are not so far distant from the slate producing districts, the British producer is more than able to maintain his own. This is strikingly brought out by the fact that no foreign slates were imported into Liverpool in 1937, whereas Leith imported 5,554 tons, practically all of which were brought across the North Sea from Norway in British colliers. This factor of transport costs is clearly of the highest importance to slate producers in their struggle with foreign competitors in the more distant borne markets and, of course, in their struggle with home‑produced and imported substitutes in the same markets.

Slate is a bulky, heavy, and comparatively fragile commodity and the cost of transportation from quarry face to house‑top has always been of cardinal importance for the industry and it is our intention in a later article to show in detail how changes in costs and methods of transport have affected the development of the industry throughout its history and to indicate the measures that are being taken, and should be taken, to over~ come the present crippling effect of high costs of transport by rail.

The great decline in the British export trade during the present century has reacted on the nature of that trade ; the quantitative change has brought with it quantitative changes.

The quantitative fall in the volume of exports has meant that the handling and shipping of British slate for foreign destinations is not now done at the small ports in the slate producing areas, but at larger ports such as Liverpool and London. Up to the last Great War most of our exports were shipped direct to the foreign markets from the Welsh slate ports. Festiniog slate mines shipped their world-famed states from Portmadoc; the numerous quarries in the Nantlle and Gwyrfai valleys shipped their slates from Caernarvon. The great Penrhyn and Dinorwic Quarries had their private ports‑Port Penrhyn and Port Dinorwic respectively.

In 1894, Portmadoc alone exported 48,700 tons of slates, of which 39,500 tons went to Germany. In 1910 Portmadoc exported 14,300 tons, of which 11400 tons went to the German market. In 1924 only 1,300 tons were exported from that port, only 200 tons being sent to Germany. These statistics serve to show what a substantial proportion of total British exports were shipped abroad direct from the tiny Welsh slate ports, and they also show the overwhelming importance of the German market. When the German demand fell off in the years preceding the last Great War the British export trade also contracted and, as the German demand did not revive in the inter‑war period and no alternative markets were found for our exports, our export trade has remained at a very low ebb.

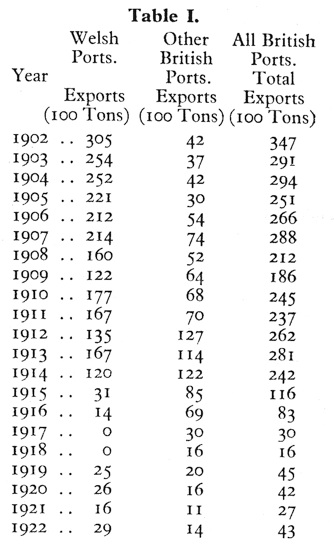

Table 1. gives the quantity of slate exported direct from the Welsh slate ports ‑ Portmadoc, Caernarvon, Port Dinorwic and Port Penrhyn ‑ for each year from 1902 to 1922, and also the quantity exported from all other British ports during those years, and the total annual volume of exports. This Table brings out two very important facts : firstly, it proves that the slate export trade was monopolised by the Welsh quarries, and that English and Scottish quarries only exported very minute quantities ; secondly, it shows the decline, both quantitatively and relatively' in the volume of slates shipped direct to the foreign market from North Wales. In 1902 some 30,000 tons were exported direct from the Welsh slate ports and Only some 4,000 tons from other British ports, so that in that year more than six‑sevenths of total British slate exports were shipped abroad from the four slate ports. This proportion was even higher for earlier years.

In 1914, however, some 12,000 tons were exported direct from the Welsh slate ports and some 12,200 tons from other ports ; for the first time in the history of the trade the quantity exported direct from North Wales was less than that sent from other ports. In the inter‑war period the tendency was for a smaller and smaller proportion of British slate exports to be sent abroad from the slate ports.

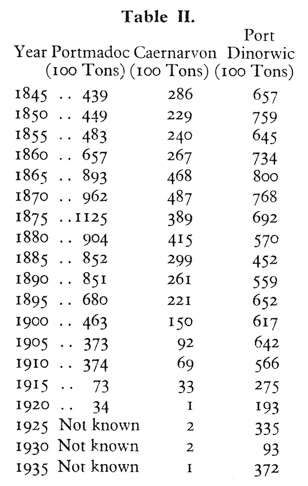

During the nineteenth century, more especially in the 'sixties and 'seventies, the Welsh slate ports were crammed with tiny little vessels waiting their turn to load with slates. The greatest number of vessels to clear out of Port Dinorwic with slate was 764 in the year 1866, an average of more than two per day all the year round. In the s3me year 735 ships cleared out of Portmadoc, again an average of two per day, Most of these romantic little ships were engaged in the coastal trade and the linking up of the Welsh slate producing areas with the general railway system proved a great blow to the slate fleet but as late as 1895 339 vessels cleared out of Port Dinorwic with cargoes of slate, and 475 vessels left Portmadoc similarly loaded. Table II. gives the quantity of slate shipped coastwise and abroad from Portmadoc, Caernarvon, and Port Dinorwic at quinquennial periods between 1845 and 1935.

Up to the last war the volume of demand for slate was such that these little vessels could still find full and remunerative cargoes but the loss of the German market spelt disaster for these little ships. The volume of shipments to other foreign markets was too small to provide cargoes and so these vessels were finally lost to the slate trade. Table IV. in our last article gave a detailed analysis of the places whence slate was exported in 1935. Total exports in that year amounted to 2,749 tons, of which 1,5 5 1 tons went to Eire and 511 tons to the Channel Islands. Trade with those two markets in the inter‑war period was largely monopolised by the Penrhyn and Dinorwic Quarries, partly because both concerns owned and operated small steam boats which enabled slates to be shipped direct from Port Penrhyn and Port Dinorwic to those markets. Even in the inter‑war period, as is shown in Table 11, a considerable quantity of slate was shipped from Port Dinorwic (the same thing applied to Port Penrhyn) in the privately-owned Dinorwic boats.

The decline of the small fleet of vessels that had so well served the Welsh slate trade for over a century, meant a great loss to the industry. These small ships had provided a very cheap means of carriage to foreign markets. After their disappearance the slate had to be sent by rail to a more distant port for shipment abroad in large cargo boats, and this more indirect method of shipment meant increased costs of handling and of transport, and this increased cost had adverse repercussions on foreign demand.

The loss of the slate boats also affected the home market. These boats had been engaged in carrying on a considerable coastal trade in slates, and had made it possible for small cargoes to be sent cheaply to the furthermost domestic markets, and so the foreign competitor had not at that time enjoyed the differential advantage he now enjoys in the form of cheaper costs of transport. The disappearance of the slate fleet meant that slate could only be sent by costly rail transport to towns along the west and north‑west coast and, as we have seen, this has played into the hands of the foreign competitor.

It is noteworthy that in the inter‑war period the quantity of slate exported to most foreign countries was very small. In 1935 1,551 tons were sent to Eire, 5 11 tons to the Channel Islands, and the other 687 tons exported in that year were sent to twenty different countries, of which twelve imported 12 tons or less. Minute quantities of this kind could only be shipped in special crates, and it is transparently clear that this sort of export trade tanks as a luxury and is not likely to expand in the future. Indeed, in many cases, the small quantities of slate that were sent out to various countries were used merely to repair buildings roofed with slate in the hey‑day of the British slate export trade, and would not otherwise have been ordered.

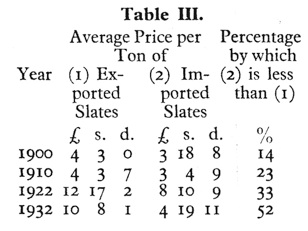

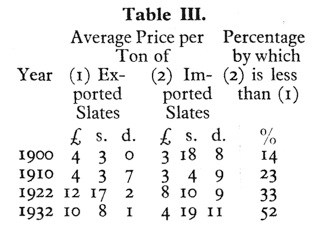

Another factor which has contributed largely to the importation of foreign slate has been the comparative price factor. It is interesting to note that ever since 1895 the average price per ton imported slates has been much lower than that of exported slates. Table Ill. gives comparative prices at various dates. It shows how the margin between the average price per ton of exported and imported slate has been growing wider and wider since 1900.

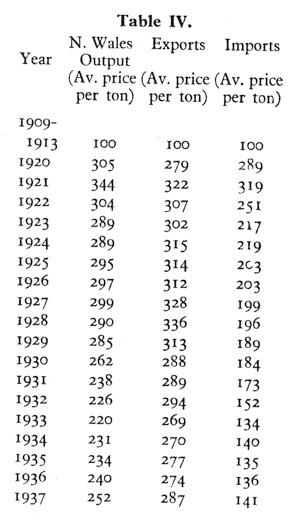

Table IV. gives an index of the average price per ton of slate produced in North Wales, of slate exports, and of slate imports, respectively for each year from 1920 to 1937, the average of the five years 1909 to 1913 being taken as 100. This Table shows that in 1937 the average price per ton of slate produced in North Wales was 152 per cent. higher than the average value per ton for the five years 1909 to 1913 ; exports were 187 per cent. higher whereas imports were only 41 per cent. higher. The statistics in Tables 111 and IV have to be very carefully interpreted because we are comparing things which are not strictly comparable. The "representative" or "average" ton of slates exported in 1937 differed from that exported in 1909 because of the qualitative changes in the export trade and also, to a smaller extent, in the import trade. Before we can really discuss the comparative price factor and its effect on British foreign trade in slate, we must have more reliable information than that contained in the above two Tables, and we propose to discuss this aspect of the problem in our next contribution.

Aspects of the Slate Industry 9: Foreign trade in slate in the present century: part 2

Quarry Managers' Journal January 1943

First series

Second series

Foreign trade 2

Third Series

Other slate information

National archive slate records

Links

Patent slating Bridestowe Devon 1795