Roofing Belfast and Dublin, 1896-98:

American Penetration of the Irish Market for Welsh Slate

A. C. Davies

Roofing Belfast and Dublin, 1896-98:

American Penetration of the Irish Market for Welsh Slate

A. C. Davies

Irish historians and economists have long recognized the importance of the construction industry as a stimulus to economic growth. Indices of house-building can offer a helpful key to understanding the way in which an economy is performing. Fluctuations in the rate of house-building directly affect other industries which supply services and materials [1]. When an economy is expanding the employment of labour and capital in these connected industries helps to sustain the upward momentum of economic activity. In most cases raw materials for building mainly because of their bulk-come from within the region in which the building occurs. Thus the effect of a building boom is usually felt locally and immediately.

Ireland, like other parts of the British Isles, shared in the building boom which reached a peak in the years 1895-98 [2]. House-building activity occurred in both rural and urban Ireland. Through the last quarter of the nineteenth century inferior housing in rural areas was replaced or improved [3]. Although the effects of this are difficult to quantify-rural house-building was a part-time occupation-they can only have been stimulating. The urban booms in Belfast and Dublin are easier to measure. In the 1890s the population of the capital increased from 245,000 to 290,000, a greater increase in one decade than in the previous half-century [4]. And the population of the northern city soared |rom 273,000 to 349,000 [5]. By the mid-nineties, Belfast had 60,000 houses, Its city boundaries had recently been increased by 11,000 acres and, one observer noted, 'if the city's prosperity and growth continues in the same ratio as at present, which is extremely probable. the numbers of structures erected will be proportionately larger’. [6] Nearly 2,300 houses were started in Belfast in 1895 and nearly 3,000 in 1896. In the same two years house building in Dublin was reported to be proceeding at about the same pace. Yet the Irish economy missed some of the benefit of its own urban growth. This was because the main supply of roofing slate carne from outside. Nearly all houses in Belfast and Dublin were roofed with slate. Even the smallest house required at least a ton (2,240 lbs), and one estimate put consumption in both cities in 1896 at 10,000 to 12,000 tons each. [7] Although there were quarries in Ireland most of the urban market for slate was supplied from North Wales. The object of this article is to explain why American and not Irish quarries filled the gap when an industrial dispute at Penrhyn in 1896-7 interrupted supplies of Welsh slate to Ireland. An incidental purpose is to illustrate the use of the United States' Consular Reports as a helpful source of information about the late nineteenth-century Irish economy.

The Irish slate industry was long established but had never been large. In 1844 Sir Robert Kane noted the existence of a handful of small concerns at Bradford in Clare, Westport in Mayo, Ross in Waterford, Clonakilty and Kinsale in Cork, and in Wicklow near Rathdrum. There were only three enterprises of more than minor importance. Quarries at Glassmore employed i00 persons, on Valentia Island about 200 persons, and at Killaloe, Co. Limerick, about 700 men and boys. The latter was originally worked by the Mining Company of Ireland, and subsequently by an English company, the Imperial Slate Company. Kane reported that it had an annual output of about 10,000 tons of manufactured slate in the 1840s, of quality which compared favourably with good Welsh slate. Other Irish slate was less suitable for roofing, but adequate for building stone or decorative purposes.[8] Despite attempts in a number of industrial exhibitions to encourage the development of Ireland's raw materials and minerals, slate quarrying remained of minor importance. [9] This was because thatch was extensively used for roofing material in rural areas, and because North wales quarries captured most of the market for roofing slate in Irish towns and cities. Slate used for purposes other than roofing-for example for billiard tables, acid baths, and school slates-amounted to fairly small quantities, and even the demand for school slate was declining. Blackboards made of slate or silicate were being replaced by ones made of wood, while individual slates were 'rapidly giving way to paper, upon which most schools do their work'. Jotters and scribblers are produced so cheaply now', one supplier reported, 'they are a much more satisfactory stock to handle', and they were more hygienic. [10]

Most Irish quarries were remote from the main centres of demand. Their handling and delivery costs placed them at a considerable disadvantage with the great welsh slate companies. Even the railway network made little difference. Indeed, railways helped the larger welsh quarries, enjoying economies of scale and greatly experienced in marketing, to penetrate to the interior of Ireland at the expense of small Irish quarries, just as within the North Wales region small welsh quarries lost their own local markets. [11] Building material, which has low intrinsic value in relation to bulk and weight, generates high handling costs if, like machined slate, it is fragile. Even though labour was cheap in Ireland, all advantage on this score was offset by greater transport costs, and by the greater incidence of breakage if subjected to lengthy land transportation. Slate travelled much more safely by sea. The north Wales coast was dotted with minor ports, connected to the quarries in the mountains by rail and tram lines, so that from the quarrying district slate could be exported easily. For the long-distance transport of bulky materials the Irish Sea was cheaper to traverse than the Irish mainland. 'Except common native stone for rubbish', noted a Dublin architect, 'it will be found that nearly all building materials in this district are more readily, cheaply and systematically delivered by sea carriage than could be obtained from native source.' [12] Loading expenses for roofing slate, the American consuls in Dublin and Belfast reported, were 24 cents a ton by vessel, and 30 cents a ton by rail-a difference of 20 per cent in favour of Welsh suppliers. [13]

Thus transport costs explain why even the largest Irish quarry, at Killaloe, was at a disadvantage against North Wales as a source of slate, for, say, Belfast; Killaloe supplied the modest demand for roofing slate from Limerick city, but not even that from Dublin. Thus it could not benefit from the steady replacement demand for slate which the metropolis generated, and was not in a position to respond to the new demand created by the boom of the 'nineties. For Killaloe and the other Irish quarries never reached the optimum size from which they might capture and hold a significant share of the market: 'the quantity offered from Irish quarries is too limited and irregular to be of much commercial importance the quarries do not give a steady or reliable supply. They are smothered by accumulations of waste and debris. They are not developed with sufficient system, capital, or under the same facilities as the Welsh quarries'.[14]

In contrast with Ireland the North Wales slate industry contained several large-scale enterprises. They had developed through the nineteenth century to supply much of the roofing slate in Britain, as well as a large market abroad. North Wales had long supplied Irish cities; [15] among Irish architects-who controlled the market through the merchants who retailed to the builders-Welsh slate enjoyed a favourable reputation for quality, price, and reliability of supply. Compared with Irish slate its quality was, according to one architect, 'decidedly superior, while the difference in price is slight'; another reported that 'as weather slates, the Welsh slates have no superior in standing Dublin climate'. Their only drawback, in the eyes of some, was their blue or purple colours - ‘cold and inartistic not generally pleasing to architects in England or Ireland'. It was less attractive than the 'really, strong, and pleasant coloured grey-green' slate from Westmorland. [16] But slate from this latter source was more expensive and until the middle 1890s price, quality, and reliability of supply together enabled Welsh slate to dominate the market in lreland and elsewhere.

In the middle 1890s these three features began to change. Io start with, quality became suspect. Sometimes even first quality slates were debased by being split too thin: 'the folly of the present Welsh quarry manipulators is in producing a thin, smooth, nice article. Close lapping with these is the worst of weather proofing - draws wet by capillary attraction and breaks under frost'. [l7] Secondly, regular supplies were no longer assured, as the North Wales quarries became the scene of prolonged and bitter industrial conflicts. This directly affected what had been the third favourable characteristic of Welsh slate - its relative cheapness. Industrial disputes at the Penrhyn quarries, which had dominated the Irish market, interrupted supplies, caused shortages in the builders' yards, and consequently a rise in price. This coincided with the increased general demand for all building materials because of the nationwide housebuilding boom. And in Dublin there was an exceptional and sudden demand for roofing slate caused by a great storm on 21 December 1894, 'when so many buildings were unroofed in the Kingdom, especially in this city'. [19] Because supply was relatively inelastic, the sudden increase in demand caused prices to rise sharply. In 1895-96 the price of Welsh slate in Ireland advanced by 30 to 40 per cent, and builders in Ireland, as elsewhere, began to look for alternative sources.

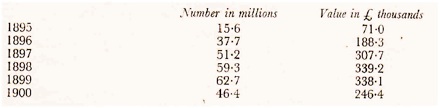

By the middle of the decade the house-building boom in Britain had induced the importation of small but increasing quantities of slate from France, Belgium, Norway, Portugal, Italy, the Netherlands, and Germany: the extent and value of this slate, for the years 1895 to 1900, can be seen in Table I.

This American dominance was partly owing to the exertion of a special company which had been formed in London to supply the metropolis with American slate. [20] And it was to the United States that Irish, Architects and merchants turned

TABLE I

Number and Value of Slates imported into the U.K., 1895-1900

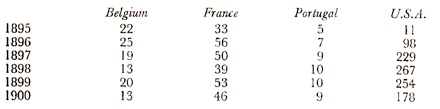

Sources: Brit. Parl. Papers, 1896, XCI (I) pp. 26-7; 1899, XCV, pp. 38-9; 1900, LXXXVI, pp. 38-9; 1901, LXXVI, pp. 32-3. The largest single source of foreign supply very quickly became the United States. By 1898 about 80 per cent of the slate imported from the main foreign sources came from that country.

TABLE 11

U.K. Imports of Slate : Main Sources and Annual Values, 1895-1900 in £ thousands

Sources : Brit. Parl. Papers: 1896, LXXXIII, p. 106; i897, LXXXVII, p. 113; 1898, XCI, p. 188; 1899, XCV, p.277; 1900, LXXXVI, p.248; 1901, LXXVI, p.245.

in the hopes of reopening an old source of supply. A small export market in slate had started in the 1870s; in Ireland it had begun with an auspicious contract for the roofing of Christ Church Cathedral in Dublin. This was covered with American Eureka Green Slate - a slate 'of excellent quality' though 'too costly for general use'. This promising opening was spoiled when 'a cheap and inferior slate resembling the other (Eureka) only in colour, was put upon the Dublin market'. It 'faded out almost white', and tended to disintegrate in the the Dublin climate. [21] American slate fell into disrepute and its export to Ireland ceased, leaving the market to Welsh suppliers. It was the possible reopening of this earlier trade following the loss of the comparative advantages of Welsh producers which attracted the attention of the United States' consuls in Belfast and Dublin in the winter of 1896-7

Even before the civil war the American consular Service had acted as a trade agency by collecting and returning to the Department of State information which might be of benefit to potential exporters. [22] Until about 1890 the nature of the trade between the United States and the rest of the world made only modest demands upon American consuls. The world's need for American raw materials required no special encouragement by her diplomats; and most American manufacturers were understandably preoccupied with exploiting their expanding domestic market. Before the 1890s the kind of commercial service provided by the consuls was more of a reporting nature, describing local conditions, than one which explicitly sought out new export opportunities. During the 1890s there was a change in attitude which can be traced through the monthly Consular Reports on economic conditions and trade openings in various consular districts. Because the spoils system determined appointments, the quality of these Reports inevitably varied. through time and place. [23] The Reports of the consuls in Ireland, however, are generally very perceptive; they offered for potential American exporters useful, and sometimes unusual, information on various facets of the Irish economy. They provided standard information about production and consumption in Irish agriculture and manufacturing, and the prospects for American exporters of raw materials, machinery, and even for quite specific products such as canned tomatoes and bicycles. They described the nature and character of local demand, what American products had been exported in the past, how they might be increased and new ones introduced, and even how shipments should be packed. The information secured by the Belfast and Dublin consuls about the market for slate in Ireland is a good example of the kind of constructive service provided by alert consuls which helps to explain the long-term change in America’s trade with the rest of the world from the 1890s.

The shortfall in the supply of slates to Ireland coincided with a surplus of slate within the United States. The American slate industry, concentrated in quarries in half a dozen states near the Atlantic seaboard, tripled its output and value of product between 1879 and 1900. [24] But the domestic market could not absorb all that it produced, and American quarries began to look for markets abroad. Several wrote to the Belfast and Dublin consuls in 1896, just at the time when Irish merchants were looking for new-suppliers. In the February 1897 issue of the Consular Reports, Newton B. Ashby, consul at Dublin, reported on the demand for slate in lreland, promised to collect more information, and to put potential sellers in touch with buyers. [25] The next issue of. the Consular Report, March 1897, included detailed reports from Ashby and from James B. Taney, the consul at Belfast. [26] These drew on information from slate distributors and architects, and from the firm of W. F. Redmond of Newry, contractors who had previously handled American imports. Redmonds were cautious about the prospects for American slates. Although they had found it easy to dispose of 1,500 tons in 1896, and although another firm had imported three lots of seventy tons, they were pessimistic about the long term: ‘once the- supply of Welsh slates again becomes equal to the demand, the importation of American slates must cease'. But Taney was more optimistic and more concerned with penetrating the present market: ‘conditions seem very favourable for an entering wedge for American slates . .' he reported, and to encourage potential American exporters he provided a detailed picture of the market for slate. [27] Taney’s Report included the prevailing price (in dollars) of Bangor and Ffestiniog slate, differences in the price of crude slate slabs compared with machined slate, the various sizes, colours and quantities shipped from Wales, their loading expenses, cost of breakage, details of methods of payment, credit, insurance, discounts, and the names and addresses of the main Irish builders' merchant - in short, a check list of relevant information needed by any potential exporters. The eleven-month Penrhyn dispute ended in mid-1897, but it was some time before production and stocks caught up with the old level. By then American exporters had successfully penetrated the Irish market. E. A. Young manager of the Penrhyn Quarries, wrote to their owner, Lord Penrhyn, [28]

'The trade as a whole continues to take every slate as fast as we can make them, but there are indications in some places that Americans are doing our market serious injury-for instance in Dublin American slates are selling at 25 per cent less than Penrhyn and we have shipped none to Dublin for over two months instead of the usual cargo a week.’

In the four years from 1897 to 1900 in excess of £125,000 worth of American slate was imported into Ireland, as Table III shows:

TABLE III

Value of Imports of Slate to Dublin, Belfast and Cork, 1897-1900

Sources: Brit. Parl. Papers, 1898,XCI, p.265; 1899, XCV, p. 303; 1900, LXXVI, p.325; 1901, LXXVI, pp. 845, 848.

During these years there seems to have been no attempt by Irish quarries to fill the gap left by Welsh suppliers. By 1901 demand for roofing slate was still high, yet the evidence of the Irish display at Glasgow International Exhibition of that year gave no indication of any expansion. [29] Twenty years later E. J. Riordan noted that Ireland still imported slate to the annual value of £100,000. [30] The reasons he offered were the conventional explanations for the retardation of the Irish economy - inadequate investment, inferior technology, and entrepreneurial failure; Irish quarries, he noted, have good quality slate, but they 'required the investment of more capital, the introduction of the best types of machinery, better transit facilities, especially in respect of rates for carriage, and general business-like management of the works'. At the time of the housing boom of the 1890s it had not been possible for these conditions to be met quickly enough to take advantage of the opening left by the Penrhyn dispute. The market for roofing slate was international. The proximity of Irish cities to the main source of British supply had inevitably left little scope for Irish quarries to develop in the nineteenth century. [31] When an opening did occur, it was American slate producers who were best able to step in taking advantage of low shipping costs, efficient selling techniques, and an alert consular service.

Queen’s University, Belfast

1 H. W. Richardson and D. H. Aldcroft, Building in the British Economy between the Wars (London, 1968), p. 270.

2 S. B. saul, ‘Housebuilding in England, 1800-1914’, Economic History Review, 2nd ser. XV (1962), 119-137.

3 J. S. Donnelley, Jr, The Land and People of Nineteenth-century Cork: The Rural Economy and the Land Question (London, 1975), pp. 242-4.

4 Census of lreland, 1901 (Brit, Parl. Papers, 1902, CXXII), p.237.Table IIa shows an increase in inhabited houses from 25,764 to 32,061.

5 Census of lreland, 1901 (Brit. Parl. Papers, 1902, CXXVI), p.189. Table II shows an increase in inhibited homes from 55,423 to 67,108. See also Emrys Jones,'Late Victorian Belfast: 1850-1900', in J. C. Beckett and R. I. Glasscock, eds. Belfast: Origin and Growth of an Industrial Cit), (Belfast, 1967) p.111

6 U.S.A., Department of State: Monthly Consular Reports, Vol LlI, No.198 March 1897: ‘Roofing Slate in Ireland’, Report by James Taney, Consul at Belfast, pp 422 to 428 -- hereafter Taney’s Report; Report by Newton J Ashbv, consul at Dublin, pp. 428 - 431 hereafter, Ashby's Report. The quotation is from Taney's Report p 422

7 Ibid. pp.422-327

8 Robert Kane, The Industrial Resources of Ireland (Dublin, 1844), pp.24l-B; George Wilkinson, Practical Geology and Ancient Architecture of Ireland (London, 1845), pp. 2l-82, and Appendix, 'Tables of Experiments on the Principal Building Stones of Ireland: Slates', which lists eighteen quarries; Thom's Irish Almanac and Official Directory (Dublin l85B), p. 228.

9 On slate in mid-century exhibitions see A. C. Davies, 'The First Irish Industrial Exhibition, Cork 1852', Irish Economic and Social History, lI (1975), 50, 56; and John Sproule, ed. The Irish Industrial Exhibition of 1853: A Detailed catalogue of its contents (Dublin, 1654;, pp. 85-96.

10 Ashby's Report, p' 429. Compare the contemporary demand for school slates in the United States - 25 million between 1895-1900-noted in J. C. Furnas, The Americans: A Social History of the United States, 1587 - 1914 (London, 1970), pp. 536-7.

11 A. H. Dodd, The Industrial Revolution in North Wales (Cardiff, 1933; 3rd ed. l97l), p.222. Cf. J. Lee, 'The Railways in the Irish Economy', in L. M. Cullen, ed. The Formation of the Irish Economy (Cork, 1969), p.82, on the effect of railways on local industries.

12 Ashby's Report, p.430. The architect continued: 'The Welsh slates have obtained nearly universal use heretofore in Dublin, simply because being a water-borne building material from the neighbouring and convenient coast, no other, subject to the greater cost and risk of breakage incident to land carriage, could hope to compete with them in price'. See also Wilkinson, op. cit. p. 28.

13 Taney's Report, p. 426

14 Ashby's Report, p. 429; Wilkinson, op. cit. p. 188.

15 Jean Lindsay (A History of the North Wales Slate Industry (Newton Abbot, 1974), pp. 192, 195) notes that Welsh slate sold in Dublin, Drogheda, Belfast, Londonderry, Dundalk, Waterford, Cork, Sligo and Letterkenny.

16 Ashby's Report, P. 430'

17 Ibid. p. 431.

18 Lindsay, op. cit. pp. 268-73; H. A. Clegg, A. Fox, and A. F. Thompson, A History of British Trades Unions Since 1889-1910 (Oxford, 1964), pp.212-14.

10 Taney's Report, P. 423.

20 Lindsay, op. cit. pp. 253-6.

21 Taney's Report, p. 423; Ashby's Report, p. 430.

22 Emory R. Johnson et al-, History of the Domestic and Foreign Commerce of the United States (Washington D.C., 1915), II, 276, 290-1.

23 On the U.S. consular service see Thomas G. Peterson, 'American Businessmen and Consular Service Reform, 1890s to 1906', Business History Review, XV (1966), 77-97, esp, 85-7; and Richard Hume Werking,'Selling the Foreign Service: Bureaucratic Rivalry and Foreign Trade Promotion, 1903-1912', Pacific Historical Review, XLV 1976), 185-207, esp. 185-8. On American business abroad in this period see Mira Wilkins, The Emergence of Multinational Enterprise (Cambridge, Mass. 1970), chs. IV and V. The several series of consular reports can be traced in British Museum, General Catalogue o printed Books (London, 1966), vol. 244, pp.445-6. A relevant discussion of the British service is D, C. M. Platt, 'The Role of the British consular service in overseas Trade, 1825-1914', Economic History Review,2nd Ser. XV (1963), 494-512.

24 Board of Trade Journal, Vol. l0 (April, 1891), pp.44.{-5; (for the 1880s): Arthur F. Burns; Production Trends in the United States Since 1870 (New York, 1934), pp. 222, 298-9; T. N. Dale, Slate Deposits and the Slate Industry in the United States (U.S. Geological Survey Bulletin 27S, Washlngton D,C., 1906).

25 Monthly Consular Reports, Vol. LIII, No, 197 (February, 1892), p. 287.

26 Loc. cit. fn. 6, supra

27 Taney’s `report, p. 422.

28 Cited in Lindsay, op. cit, p. 253.

29 G. A.J. Cole,'Irish Minerals and Building Stones', in W. P. Coyne, ed. Ireland: Industrial and Agricultural: Handbook for the Irish Pavilion Glasgow International Exhibition, 1901 (Dublin, 1901), p. 25.

30 E. J. Riordan, Modern Irish Trade and Industry (London, 1920), pp. 148-9.

31 The output of Irish slate quarries remained low until the 1930s. Then, protected by a massive tariff of £5 a ton, imports declined (from 7,000 tons in 1930 to 1,800 tons in 1938) and domestic output increased (from 6,400 tons in 1931 to 14,200 tons in 1936). See Saorstat Eireann, Trade and shipping statistics (for 1930 and 1939’ Dublin 1931and 1939); and Department of Industry and Commerce, Irish Trade Journal and Statistical Bulletin (December, 1937), p. 236. (I am grateful to Mr D. S. Johnson for these references.)

First series

Second series

Third Series

Other slate information

National archive slate records

American slate in Ireland

Links

This account of the opportunity seized by American slate producers during the Penrhyn Quarry dispute of 1896-1897 was published in The Journal of Irish Economic and Social History, Volume IV 1977.

I am grateful to Dr Davies and the Society for permission to reproduce it.

Dr Davies was formerly head of the Department of Economic and Social History, Queen’s University, Belfast.